Maintaining a valid NBFC license in India requires strict adherence to regulatory norms set by the Reserve Bank of India. With increased scrutiny in 2026, the RBI has become more proactive in cancelling licenses of NBFCs that fail to comply with essential guidelines. This blog highlights the most common reasons behind license cancellations and how businesses can safeguard themselves through proper compliance and governance.

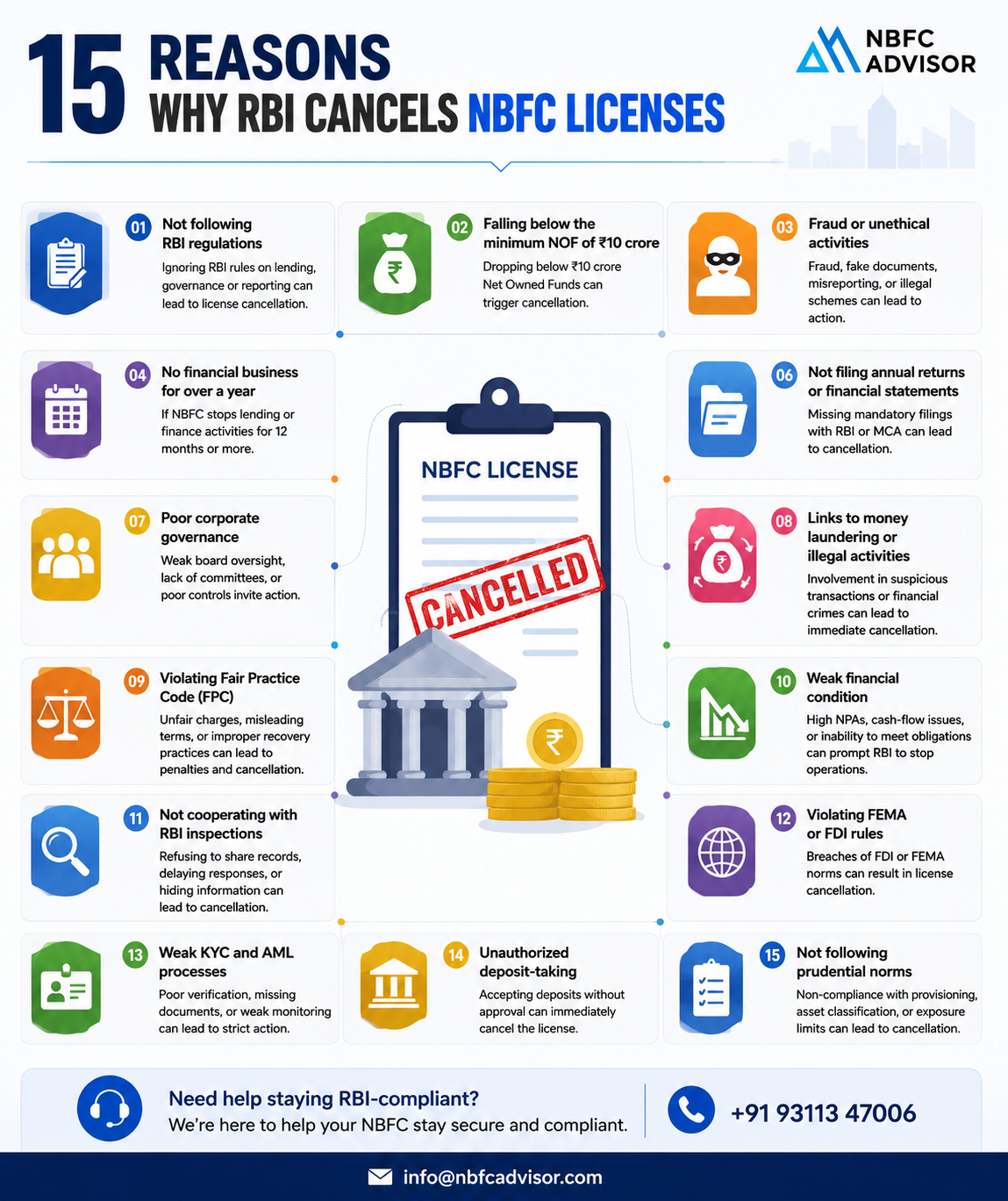

One of the primary reasons is non-compliance with RBI regulations, including violations in lending practices, governance, and reporting standards. Failure to follow prescribed norms can quickly attract regulatory action.

Another critical factor is falling below the minimum Net Owned Fund (NOF) requirement. NBFCs must maintain the required capital threshold to continue operations, and any shortfall can trigger cancellation proceedings.

The blog also addresses fraudulent or unethical activities, such as misreporting, fake documentation, or involvement in illegal schemes. These actions lead to immediate and strict regulatory penalties.

Operational inactivity is another risk—NBFCs not conducting financial business for over a year may lose their license due to non-utilization. Similarly, failure to maintain the required Capital Adequacy Ratio (CAR) can impact financial stability and lead to regulatory intervention.

Non-filing of returns and financial statements is a common compliance lapse that can result in serious consequences. Timely reporting to RBI and MCA is mandatory for continued operations.

Weak governance structures, poor internal controls, and lack of transparency in operations also contribute to regulatory risks. NBFCs must maintain proper board oversight and ensure accurate disclosures.

Other major triggers include:

- Links to money laundering or suspicious activities

- Weak financial health and high NPAs

- Violation of Fair Practices Code (FPC)

- Non-cooperation during RBI inspections

- Weak KYC/AML frameworks

- Unauthorized deposit-taking activities

- Violation of FEMA/FDI regulations

- Ignoring prudential norms and asset classification rules

Key Services Covered:

- NBFC Compliance & RBI Advisory

- KYC/AML Framework Setup & Review

- Financial Health & Capital Adequacy Assessment

- Regulatory Filings & Reporting Support

- Risk Management & Internal Control Systems

- Governance & Audit Readiness

- FEMA/FDI Compliance Advisory

This blog emphasizes that license cancellation is often the result of avoidable compliance failures. By implementing strong governance, maintaining financial discipline, and ensuring timely regulatory reporting, NBFCs can significantly reduce risks.

Overall, this blog serves as a practical guide for NBFCs to understand critical compliance gaps, take corrective actions, and operate confidently within RBI regulations, ensuring long-term stability and growth.