Non-Banking Financial Companies (NBFCs) operate under a strict regulatory framework governed by the Reserve Bank of India. With increasing scrutiny and rising penalties, it has become essential for NBFCs to adopt a proactive compliance approach. This blog explains key RBI regulations, common risk areas, and how NBFCs can avoid warnings and penalties while ensuring sustainable growth.

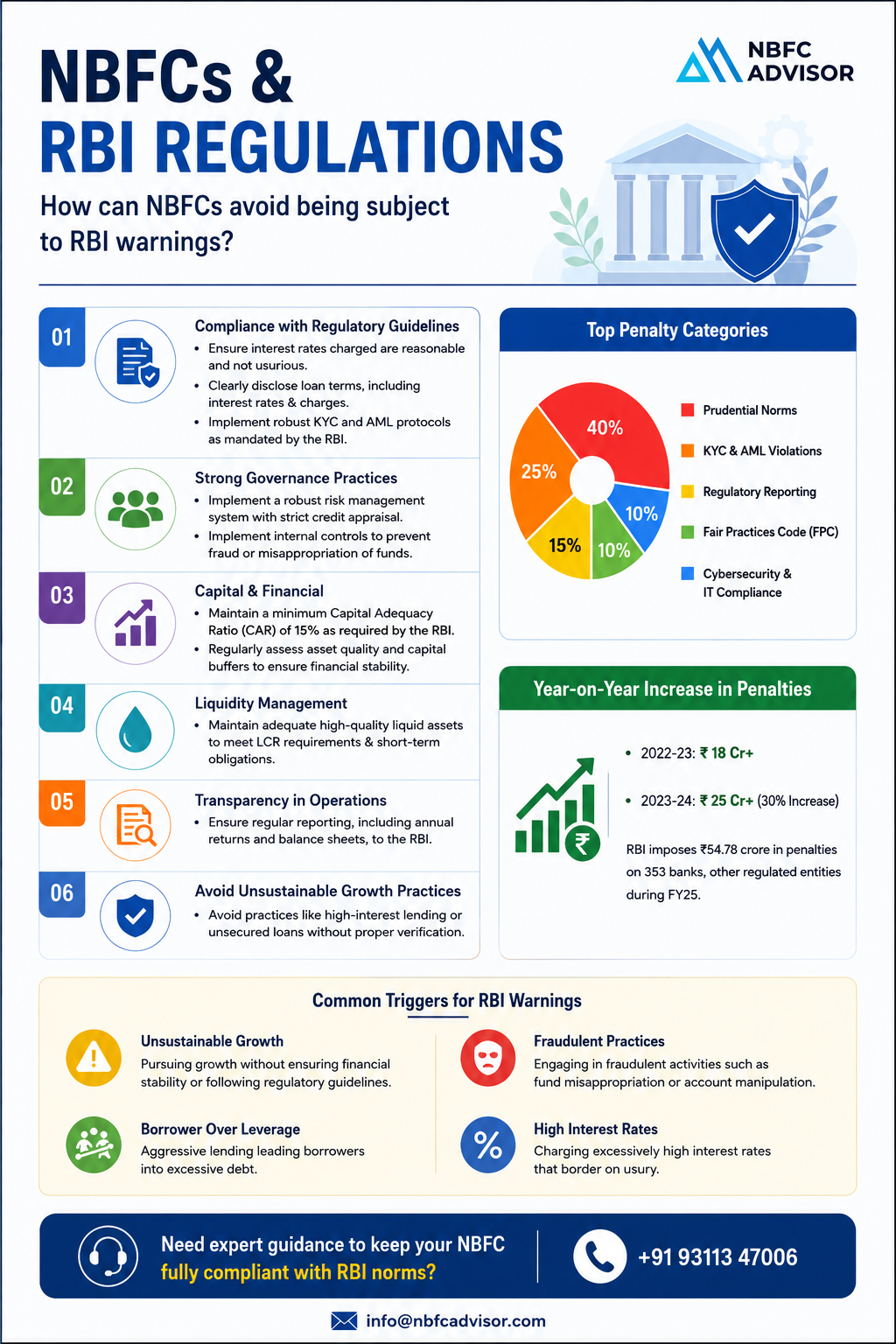

A critical aspect of compliance is adhering to regulatory guidelines, including fair interest rate practices, transparent loan disclosures, and strict implementation of KYC/AML norms. These measures not only ensure regulatory compliance but also build customer trust and credibility.

The blog also emphasizes strong governance practices, where NBFCs must implement robust internal controls, risk management systems, and board-level oversight. Effective governance helps prevent fraud, mismanagement, and operational inefficiencies.

Another key area is capital adequacy and financial discipline, where NBFCs are required to maintain a minimum Capital Adequacy Ratio (CAR) and regularly assess asset quality. This ensures financial stability and resilience against market risks.

Liquidity management is equally important, requiring NBFCs to maintain adequate liquid assets to meet short-term obligations and comply with Liquidity Coverage Ratio (LCR) norms. Poor liquidity planning can lead to regulatory actions and operational challenges.

The blog also highlights the importance of transparency and timely reporting, including accurate submission of financial statements, returns, and disclosures to RBI. Delays or discrepancies in reporting are among the most common triggers for regulatory warnings.

Additionally, NBFCs must avoid unsustainable growth practices, such as aggressive lending, high-interest rate charging, or inadequate credit checks. These practices not only increase risk but also attract regulatory scrutiny.

Common Triggers for RBI Warnings:

- Rapid growth without financial stability

- Weak credit risk assessment and borrower over-leverage

- Fraudulent practices or fund mismanagement

- Charging excessively high interest rates

- Non-compliance with reporting and disclosure norms

Key Services Covered:

- RBI Compliance & Regulatory Advisory

- KYC/AML Policy Implementation & Review

- Risk Management & Internal Control Frameworks

- Capital Adequacy & Financial Health Assessment

- Regulatory Filings & Reporting Support

- Governance & Audit Readiness

This blog highlights that compliance is not just about avoiding penalties—it is about building a stable, transparent, and growth-oriented financial institution. With the right advisory support, NBFCs can strengthen their compliance frameworks, mitigate risks, and operate confidently within RBI regulations.

Overall, this blog serves as a practical guide for NBFCs to understand regulatory expectations, avoid common pitfalls, and ensure long-term success in a highly regulated financial environment.